Abstract

Reducing the maintenance costs associated with street trees may increase initial costs for preventive treatments. Three measures are described to help you decide if investments in preventive measures are justified by future savings in reduced maintenance: present discounted values, internal rates of return, and service-life extension values. The measure you use will depend on your objectives and on the funding and accounting practices and philosophy of your organization.

Preventive measures may substantially reduce costs of street tree maintenance such as pruning roots, repairing sidewalks, and pruning branches for power line clearance or safety. For example, devices to control root damage to sidewalks have been commercially available for years. Planting stock that is slower growing or deeper rooting, or that is grown in deep containers may also reduce such damage. Managers, however, need some basis for judging whether preventive measures are worth their cost.

Cost-saving treatments cannot be rated categorically because maintenance costs depend on the species or varieties used, how they are grown and planted, the growing space and conditions provided, soil and drainage characteristics, and other site-specific factors. Three procedures, however, permit you to estimate how much to invest for future benefits: the discounted present value of future benefits, the internal rate of return, and service-life extension value (useful-life value). The first two methods are standard approaches used by economists for cost-benefit analysis (1). The third is a simple, common-sense approach. All three require reasonable estimates of costs and the duration and amount of expected benefits.

Present Discounted Value

Money is almost always worth more to economically rational people today than at some future date. Consequently, they will defer immediate use of their money only if compensated, usually by interest payments. In effect, a sum spent in the future is equal to a lesser sum spent now. The longer you must wait to use money, the less is its present discounted value. Time preference for the value of money can be expressed as a rate of interest (discount rate).

The influence of time on relative values is so great that economists insist that sums spent at different times be adjusted to their value at some common time before they can be compared with validity. Computations of present value are used extensively by economists and accountants to compare the worth of alternative investments when costs and benefits occur at different times. To obtain its present discounted value (PV), a future sum (FV) is discounted by a compound interest rate (r) using the formula

where N equals the number of years in the future.

where N equals the number of years in the future.

Table 1 gives present values for each $100 that would be spent on maintenance for a range of future times and interest rates. For example, if $500 of maintenance will be needed 10 years hence and the interest (discount) rate is 5%, the present value of that sum is $305 ($61 × 5). If something you can do now will delay the need for the $500 of maintenance for another 5 years (i.e., for a total of 15 years), the present value of that amount wil be $240 ($48 × 5). In other words, at a 5% interest rate, spending $500 in 15 years would be equivalent to spending $240 now. If $500 of maintenance would normally be needed in 10 years, you could (at 5%) afford to spend nearly $305 on any measure that would permanently eliminate this maintenance cost. If, however, the maintenance reduction measure would only delay the $500 expense so it occurred in 15 years, you could afford to spend only $65 (the difference between $305 and $240) to postpone the maintenance.

Present value per $100 of future maintenance costs (rounded to the nearest dollar).

Internal Rate of Return

Because choosing and justifying the interest rate is often difficult, an alternative to computing present discounted value is computing the rate of return that a contemplated investment would provide. You would prefer an investment returning 12% rather than one returning 8%, other things being equal.

The internal rate of return is the compound interest rate that equalizes the present discounted value of costs and benefits. If applying a single treatment would avoid annual maintenance costs for N years, you would solve the following formula for the interest rate (r) at which the present value of the series of annual savings would exactly equal the cost of a single investment (I) made now:

When investments postpone rather than eliminate costs, the present values of costs and benefits are needed to calculate internal rates of return. For example, if an investment (I) at the time a tree is planted would delay the usual costs of repairing sidewalk damage at 15, 20, and 25 years (treated as benefits (B) because they are avoided at the time usually needed) with costs (C) at 22 and 30 years, the generalized formula would be B15 + B20 + B25 = I + C22 + C30. The specific formula would be that shown in Fig. 1. Again the internal rate of return is obtained by solving for r.

Formula (example) for calculating postponed investments.

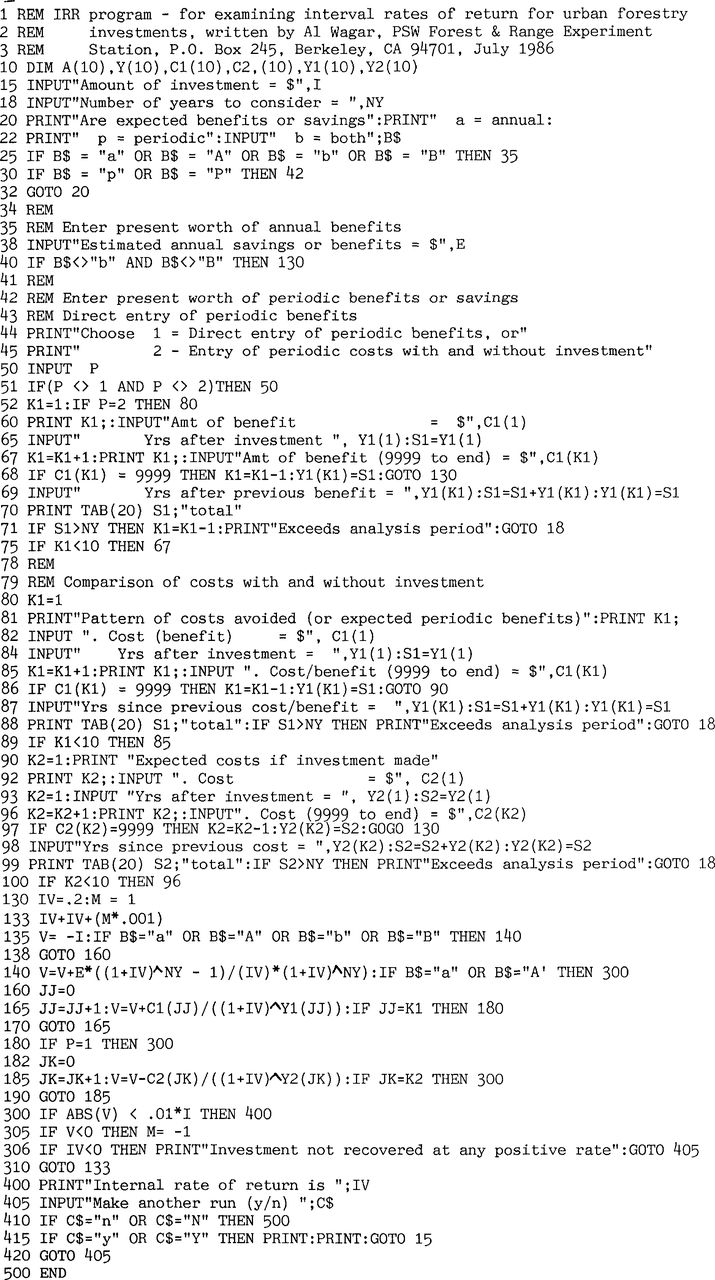

Although the general concept of internal rate of return is fairly straightforward, computation can be tedious, requiring repeated computations trying different interest rates until the correct one is found. Fortunately, successive approximation problems are readily solved using a computer. Hand-held calculators designed for business or financial applications usually have a special function key for determining the internal rate of return. Options for determining the internal rate of return are provided for in most financial software for personal computers. A program listing for calculating an internal rate of return adapted to urban forestry decisions is given in Figure 2. Table 2 gives some example scenarios and their rates of return, using that program. A graphical, linear interpolation method for estimating the rate in simple cases is given in (2).

Internal rates of return for selected treatment scenarios.

The internal rate of return can be calculated with this computer program for comparing alternative urban forestry investments. It is written in Microsoft BASIC for IBM PC and compatibles. (Trade names are used solely for information, and imply no endorsement by the U.S. Department of Agriculture.)

Service-Life Extension Values

Another way to determine how much you should spend on maintenance prevention measures is to consider that the benefit produced by delaying maintenance for a year is worth the maintenance cost divided by its normal service life. For example, if $500 of maintenance work normally is needed every 15 years, each year of service-life is worth approximately $33. If a protective measure will extend the service life by 5 years, the savings will be $165 ($33 × 5). Therefore, you could justify spending up to this amount on protective measures. If a measure extends the maintenance interval by only 3 years then only a $99 cost ($33 × 3) is justified. Expressing benefits as service-life extension values provides a different, but useful, perspective on cost thresholds for protective measures. Service-life extension values are easily calculated without formulas, but do not consider individuals’ preference for present over future values. The amount you can justify spending increases rapidly and in direct proportion to how much an expenditure extends normal maintenance times.

Choosing A Method

The measure of economic efficiency you should use depends on your objectives and on the funding and accounting practices and philosophy of your organization. How does it evaluate budgets and allocate funds among departments? Does it support an increase in current spending to reduce future expenditures on repairs? How does it allocate funds between maintenance, repair, and capital improvement? Even if your budget requests are not analyzed and funded by comparing savings with costs, you still should analyze your own priorities using some economic efficiency criteria.

If allocation of funds is based, in whole or part, on standard economic analysis, use present discounted value or internal rate of return. If your organization’s budget analysts use an interest rate to compare costs and savings, use that rate and present discounted values. Alternatively, you might want to use the interest rate your city pays for borrowing operating funds until the tax revenues roll in, the rate it pays on bond issues, or the average commercial rate for borrowing money. If allocation of funds is determined (or influenced) by where returns on investments are greatest, use the internal rate of return for your analyses. If alternative budget allocations are compared by using a nonstandard economic method, you may want to use the service-life extension method because it is simpler to do, to comprehend, and to explain.

Showing some measure of the economic efficiency of alternative expenditures in your budget might greatly help you gain support for budget requests.

- © 1987, International Society of Arboriculture. All rights reserved.

In this issue

{kind=link}

{kind=link}

Jump to section

Related Articles

Cited By...

- No citing articles found.